Pros and Cons

Original Medicare & Plan F

Pros:

- Covers remaining 20% of Medicare A & B

- Any doctor Any hospital that accepts Medicare nationwide (No Networks)

- No referral needed to see a specialist

- No deductibles, No coinsurance, No copays

- You can switch to another Medicare Supplement plan anytime of the year

- Guaranteed renewable as long as premiums are paid

Original Medicare & Plan G

Pros:

- Covers remaining 20% of Medicare A & B

- Any doctor Any hospital that accepts Medicare nationwide (No Networks)

- No referral needed to see a specialist

- $226.00 annual deductible, No coinsurance, No copays

- You can switch to another Medicare Supplement plan anytime of the year

- Guaranteed renewable as long as premiums are paid

Medicare Advantage Plans (Part C)

Pros:

- Combines Medicare A, B and usually D

- $0.00 to $100.00 monthly premiums depending on the plan you choose

- Drug plan usually included

- Dental, vision and hearing usually included

- Silver sneaker benefit on most plans

- No underwriting

Cons:

- Average Monthly premium ranges from $135.00 to $250.00 and up

- Rate increase averages 10 to 12% each year

- Thorough underwriting needed to switch plans at age 66 and over

- Drug, dental, vision and hearing plan not included on most plans

- Plans will no longer be offered to anyone Medicare eligible starting Jan 1, 2020

Cons:

- Average Monthly premium ranges from $90.00 to $120.00 and up

- Rate increase averages 1 to 3% each year

- Thorough underwriting needed to switch plans at age 66 and over

- Drug, dental, vision and hearing plan not included on most plans

Cons:

- Must stay in Network for coverage (No coverage outside of network unless emergency room visit)

- Plan can drop anytime during the year

- Providers can leave the network anytime during the year

- Referrals are usually required to see a specialist

- Copays, coinsurance, and deductibles apply

- Up to $8,300.00 max out of pocket depending on the plan

- 1-year minimum contract plan

- Prior authorizations needed for certain procedures

Tips to Follow

Choosing a Medicare plan that meets your needs is crucial as not having the proper coverage can greatly impact how much you will pay. Without the proper coverage, you could be paying thousands of dollars out-of-pocket.

To avoid this mishap, here are some tips you can follow when deciding between plans:

- If you have a preferred primary care doctor that you go to, ask them what type of Medicare plans they accept. Do they only accept Original Medicare? Medicare Advantage? If they accept Original Medicare, you can most likely stick with them as your primary care doctor. However, if you opt to enroll in a Medicare Advantage Plan, be advised that some Advantage Plans will require you to receive care within their network. This means that if your doctor is not in the network, but you still choose to receive their services, you could end up paying for most, if not all, of your medical costs.

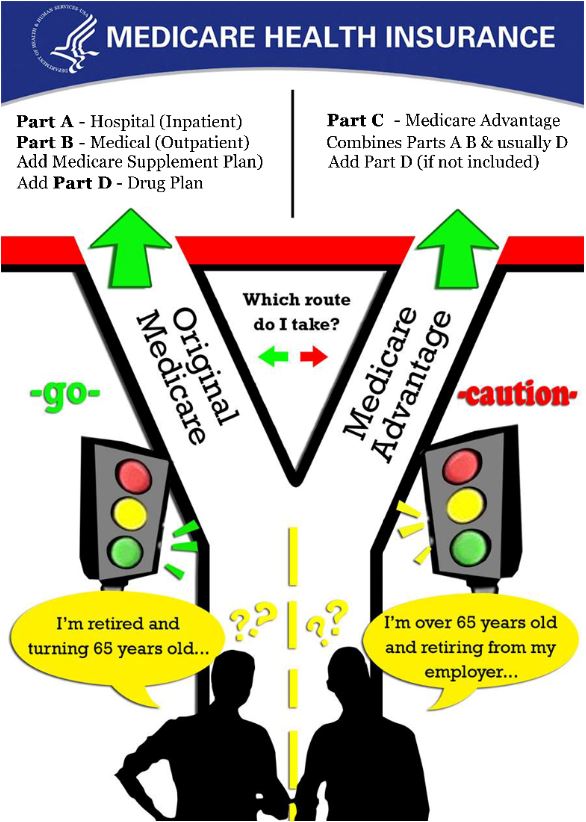

- Speaking of Original Medicare and Medicare Advantage, you need to decide which of these plans you want to enroll in. Of course, you will need to enroll in Original Medicare first before enrolling in Medicare Advantage, but it’s up to you to figure out which plan will provide the coverage you need most. With Original Medicare, you can stick with Part A (inpatient) and Part B (outpatient) coverage. Whereas with Medicare Advantage, you get both Part A and B coverage and extra benefits, including dental, vision, hearing, and prescription drug coverage.

- If you do a lot of frequent traveling, especially outside the United States, it would probably be best to look into a Medicare Supplement Plan. Plans C, D, F, G, M, and N are the only supplement plans that cover up to 80% for foreign travel emergency care.

- Take a look at each plan’s premium rates and the coverage they offer. Typically, the higher the premium, the more coverage you receive. The lower the premium, the less coverage you receive. It’s ultimately up to you if you want more coverage or would rather have a lower premium.

- Consider a Medicare Part D plan, also known as the prescription drug plan. If you take prescriptions and are looking for prescription drug coverage, it’s important to check the formulary of the Part D plan you’re considering to ensure your prescriptions are covered. A Part D plan can certainly save you from spending a ton of money out-of-pocket, but this plan isn’t always for everyone.

- Keep track of enrollment periods. Enrollment periods are your saving grace when it comes to avoiding late enrollment penalties. When you first become eligible for Medicare, you will be put into an Initial Enrollment Period that lasts six months. You can work with a Medicare agent from Great Nation Insurance, free of charge, to properly examine what coverage you need and how to enroll on time if you’re not automatically enrolled. However, if you wait longer than the initial six months to enroll, you will have permanent penalties added to your premiums. Granted, there are other enrollment periods to look into, such as the General Enrollment Period, but you still may have penalties.

Speak With An Agent Today

At Great Nation Insurance, we care about finding the coverage that meets your needs the most. Give us a call today so we can help you take that next step in finding you a Medicare plan.

Get Your free Quote

- Free Consultation

- Speak To An Agent

- Get A Quote Now

We are not connected with or endorsed by the United States government or the federal Medicare program.